Esc-Clermont Sup de Co

2nd

years, 1st semester

Course :

Corporate finance

Teacher :

André Cabannes

Please write your

name in this box :

Final exam & Answers in blue

December, 2007

3 hours, 20 questions, each worth 5 points. Write

your answers on this document in the blank space below each question.

Question

1: At the end of

its accounting year, and after including year end adjustments, a firm has the

following trial balance:

|

|

Debit |

Credit |

|

Capital |

|

100 |

|

Cash |

10 |

|

|

Opening stocks (IS) |

- |

|

|

Closing stocks (IS) |

|

50 |

|

Closing stocks (BS) |

50 |

|

|

Equipment (fixed

assets) |

50 |

|

|

Mary (supplier) |

|

- |

|

Purchases |

80 |

|

|

Salary |

10 |

|

|

Sales |

|

90 |

|

Steve (client) |

40 |

|

|

Depreciation (IS) |

10 |

|

|

Cumulated deprec. (BS) |

|

10 |

|

Provisions (IS) |

20 |

|

|

Cumulated prov. (BS) |

|

20 |

|

Total |

270 |

270 |

On the following page, establish its Income

Statement, and its Balance sheet.

This

question was treated in the course:

http://www.lapasserelle.com/clermont/corporate_finance/Lesson3/review.htm

1) Profit and loss account

|

|

Debit |

Credit |

|

Sales |

|

90 |

|

Op stocks |

- |

|

|

Purchases |

80 |

|

|

Cl stocks

(IS) |

|

50 |

|

Salary |

10 |

|

|

Dep (IS) |

10 |

|

|

Prov (IS) |

20 |

|

|

P&L |

|

20 |

2) Balance

sheet

Assets

|

|

Debit |

Credit |

|

Equipment |

50 |

|

|

Cum dep |

|

10 |

|

Cl stocks |

50 |

|

|

Clients

(Steve) |

40 |

|

|

Cum

provisions |

|

20 |

|

Cash |

10 |

|

|

Total |

150 |

30 |

Liabilities

|

|

Debit |

Credit |

|

Capital |

|

100 |

|

Cum

P&L |

|

20 |

|

Suppliers

(Mary) |

|

- |

|

Total |

|

120 |

Question

2: Is the asset

side of the balance sheet of a firm the list of all the values today of what the firm owns?

(explain)

No.

The asset side does record what the firm owns, but at acquisition value, which usually

is not the same as the values today. This is particularly true of land assets.

Question

3: A firm sells for 120€, cash, an item recorded

at 90€ in its stocks: show the impact of this operation on the balance sheet.

Cash

increases by 120€

Stocks

decrease by 90€

So

the asset side increases by 30€

And,

on the liability side, this corresponds to an increase of 30€ in the cumulated

profit.

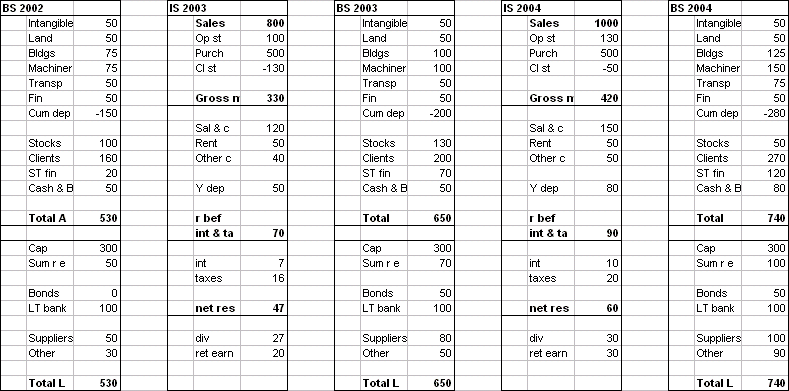

Consider

the following year end documents of a firm. Questions 4 and 5 refer to these

data (example from lesson 3a, section “an example over two years”):

{kind=link}

Question

4: What is the ROCE

ratio in 2003 and in 2004 ?

First,

let’s compute the Capital engaged :

CE2002 = 300 + 50 +

0 + 100 = 450

CE2003 = 300 + 70 + 50 + 100 = 520

CE2004 = 300 + 100 + 50 + 100 = 550

The average CE in 2003 is (450 +

520)/2 = 485

The

average CE in 2004 is (550 + 520)/2 = 535

ROCE

= (Result before interest and taxes)/(average CE)

So

ROCE2003

= 70/485 = 14,4%

ROCE2004

= 90/535 = 16,8%

(This

was also a question treated in the course.)

Question

5: What do we mean

by “this firm doesn’t use much its free financing possibilities”?

We

mean that its current liabilities are “too low” compared to its current assets.

In other words, the firm could have higher current liabilities (pay with a

longer delay its suppliers), and reduce the amount of money borrowed from banks

and bond holders, which is costly.

Question

6: What

distinguishes General Accounting and Cost Accounting?

General

accounting is

-

Turned toward the past

-

Legally required

-

Must be published

-

Very global

-

Useless for day to day management

Cost

accounting is the opposite on each criterion. It is

-

Turned toward the future (used to prepare

budgets)

-

Not mandatory

-

It is advisable not to publish it (which would be

very valuable for the competitors)

-

Very detailed

-

Very useful for day to day management (this is

why it is sometimes called “managerial accounting”)

Question

7: What is a cost

center? What is a profit center?

A

cost center is a small part of the activity of the firm where costs of the same

nature are accumulated. Usually they are under the responsibility of a low

ranking manager, or a supervisor. For instance, the “salary costs of welding in

the children bike product line” is a cost center.

A

profit center is a large part of the activity of the firm to which we can

assign a part of the sales, and therefore of the profit (or at least of the

contribution before non allocated costs).

Question

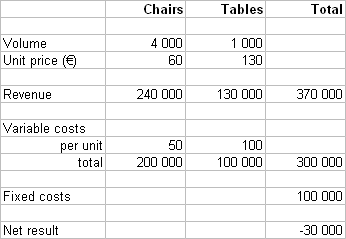

8: A manufacturer

of furniture has the following income statement, split by product lines :

(It looses

money.)

For what

pairs of unit prices would it make money?

Exercise

done in class.

Observe

that the pair of prices (100, 0) turns a profit of zero.

And

so does the pair (0, 400).

In

a two dimensional plan with abscissa, the price of chairs, and ordinate, the

price of tables, draw the line joining these two points.

Any

pair of prices on or above the line, is OK.

Question

9: Why are complete

unit costs artificial? Yet, why are they useful?

Complete

unit costs are artificial because they encompass artificial allocations of

fixed costs.

Yet,

they are useful to establish a sensible price list.

Question

10: You are the

general manager of firm A. You consider buying firm B. You would pay the

shareholders of B a certain price, and would take over all the debts and other

credits of B.

How would

you approach the question of figuring how much money to pay for B?

This

is akin to a physical investment. The acquisition will have an impact on our

other activities. Therefore we must look at the future cash flows without the

acquisition, and the future cash flows with the acquisition.

The

stream of extra cash flows (estimated), properly discounted, will give an upper

limit to the price to pay for B.

Question

11 : Consider a

security S which can be purchased today. In one year, it will have a value X

which is random (depending upon the state of the economy). The possible values

of X, with their respective probabilities, are given in the following table:

|

Possible

outcomes |

90 € |

100 € |

110 € |

120 € |

130 € |

140 € |

|

Probabilities |

10% |

15% |

25% |

25% |

15% |

10% |

If a money management

fund purchases S today, for a price P, how will it record this transaction in

its accounting system? (Debit and Credit.)

We

debit one of the “securities accounts” of the management fund, and we credit

whatever account was used to pay.

Question

12: What is the

expected value of S in one year? (Explain your calculations.)

115€

(weighted average of the possible values, weighted with the probabilities)

What is the

standard deviation of the value of S in one year? (Explain your calculations.)

Variance

= 205 (formula: average squared deviation around 115)

Standard

deviation = 14,3€ (square root of the variance)

Question

13: In the euro

zone, in early December 2007, the rate of return of a risk free security is 4%.

What is the price today of a risk free security that will be worth 115€ in one

year?

115/(1

+ 4%) = 110,58€

Is S (of

question 11) risk free?

No,

because the value of S next year is not fixed. It is a random variable with

some variability (measured, for instance, by its standard deviation).

Question

14: Suppose S sells

today for a price P = 90€. What is the expected profitability of S?

(115

– 90) / 90 = 27,8%

Question

15: What is the “risk-return

graph” that helps describe a financial market?

A

plot in two dimensions (with the risk in abscissa, and the expected return in

ordinate) of the securities available in a given market.

Return

= (Future value – Price) / Price

Risk

= standard deviation of Return

Question

16: Explain the

concept of present value. Use the following example: why a sum of 100€ promised

in one year is not worth 100€ today? What happens to its present value if its

future value is risky?

The

promise, held today, to receive a certain amount of money M, in one year, has a

value today, which is somewhat less than M. It depends upon the risk of M (if

it is a random variable); but even the promise of sure future payments are

worth less than their “face value”.

Why

is that? It is so because, when we buy the promise, we give up the possibility

to “make our money work” (in a physical investment for instance). So we cannot

pay M (the future value) for the promise.

The

more risky is the future payment M, the smaller is the price today.

This

is the reasoning in the Modern Theory of Finance (i.e. the standard theory at

present). It is not devoid of subtle paradoxes.

Question

17: We are

considering making an investment I, which will produce the following cash flows

in the future for us:

|

(mio

euros) |

year 0 |

year 1 |

year 2 |

year 3 |

year 4 |

|

|

|

|

|

|

|

|

Future

cash flows |

|

50 |

100 |

130 |

80 |

Suppose

this investment has the same risk pattern as S above, i.e. its opportunity cost

of capital is r = 27,8%. What is the Present value of the stream of future cash

flows of I? (Show your calculations.)

Use

the discounting formulas taught in class.

The

present value of the cash flow C1 (50 in one year) is PV(C1) = 39,1

PV

(C2) = 61,2

PV

(C3) = 62,3

PV

(C4) = 30,0

So

the present value of the whole collection is: 39,1 + 61,2 + 62,3 + 30,0 = 192,6

If we can

make this investment with an initial cash-flow-out of 200 millions euros to be

spent year 0, is it a good investment?

No,

because this is higher than the value today of what we buy (the present value

of the stream of future cash flows).

Question

18 : Explain what

we mean by the IRR of an investment.

For

a given C0 (the initial investment we have to make to “acquire” or produce the

stream of future cash flows), it is the value of the discounting factor that

makes the Net Present Value equal to zero.

It

is a generalisation of the concept of profitability.

Suppose we

can make I with CF year 0 = 200 mio euros. What is the NPV of I, if the proper

discount rate (i.e. the opportunity cost of capital) is 20%?

NPV

at 20% = 24,9

What is the

NPV if r = 30%?

NPV

at 30% = -15,2

Estimate

the IRR of I.

The

exact result is: 25;8%

It

can be obtained approximately using a linear interpolation between 20% et 30%.

Question

19: What is the

central idea introduced by Finance which distinguishes it from Accounting?

“The

time value of money”.

That

is, more explicitly, the idea that a promise, held today, to receive a sum of

money M in say one year, has a value today which is less than M.

This

is so, because by spending money to acquire the promise, we abandon the

possibility to “make it work” in a physical investment. So if we paid M, we

would abandon the possibility to have more in one year.

Question

20: You have in

your pocket a $1000 face value 7 year 5% coupon rate bond, that you bought two

years ago. It has five years more to go. Today’s going rate for new 5 year

bonds is 4%. What is the value of the bond you have in your pocket?

We

must discount with 4% the five future cash flows (50, 50, 50, 50, 1050).

This

yields : $1044,52